How can I manage my money better?

Now there’s a question that many households will ask, especially at the end of the month. A recent study found that one in four French people regularly find themselves in the red. Whose fault is it? There are always unexpected expenses, but, without a doubt, there is a lack of economic and financial education. Who is teaching us to distinguish between investment and consumer spending? To calculate compound interest? To work out our basic requirements? Or simply to know our way around savings and investments? Apparently not many people…But solutions do exist.

Kakebo: the Japanese method for managing your budget (and saving)

You may not have heard of it, yet the Kakebo method (or Kakeibo meaning ‘account book’ in Japanese) has been used for centuries. Children in the land of the rising sun are given these books from an early age to familiarise them with budgeting as quickly as possible. What makes Kakebo unique? It’s simple: more than just an accounting or reporting tool, the method emphasises savings. It is based on a classification of expenses into just 4 categories (general expenses, pleasure, culture and extra). After each purchase, you classify the spend in each category, and, most importantly, take stock at the end of every month: how much money do you have at the end of the month? How much are you really spending? And how much could you be saving? The aim is to set objectives to reduce spending and, of course, to create savings. The method is simple to set up and is easily accessible (Kakebo tables are readily available for free on the internet), but it does require an investment of time and tenacity.

What apps are available to help manage your budget?

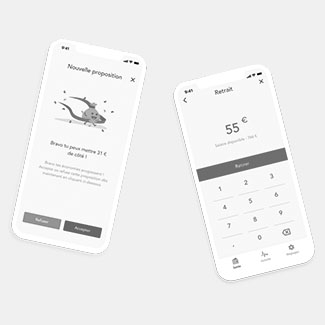

If filling in tables is not your thing, don’t worry: there are apps for that! Relying on artificial intelligence, there are able to analyse your spending habits and the movements in your accounts to determine your profile and then help you to optimise your budget. Let’s take a look at BANKIN’. Launched in 2011, the app is the first in Europe to have received approval from the French Prudential Supervision and Resolution Authority (ACPR), which is responsible for monitoring the conduct of banks and insurance companies. It already enables nearly 3 million users to keep track of their spending, to forecast their balances and even receive personalised investment and mortgage offers. A true banking advisor in your pocket.

From savings and budget management to automation.

Other apps offer you the chance to go one further. Take the example of BRUNO. Described as the ‘financial wellness app’, it analyses your spending, anticipates your movements and puts some money aside for saving. Every week, the app sends you a message inviting you to put the money in a 1% interest savings account called ‘the Bruno account’. 60,000 users are already converted. It costs them €2.99 per month to access their account, piggy bank and salary as well as giving them free deposits and withdrawals. After ethical saving and savings that build with your spending to finance your children’s studies, now it’s time for the automated version, saving without even having to think about it!

An educated consumer is a responsible consumer.

If this education continues and broadens its scope, it will undoubtedly have an impact on consumer habits and therefore potentially on retailers. So why be satisfied with seeing just the product price? Perhaps we also need to see the cost in relation to the product life, the number of times it is uses and its upkeep costs.

The better-informed consumer could also be interested in data that presents alternatives such as long or short term rental. There’s a good chance that brands know how to support their customers in their financial decisions and will create an image for themselves as responsible retailers.

Crédit : iStock, Bankin, Hibruno, Operation Business